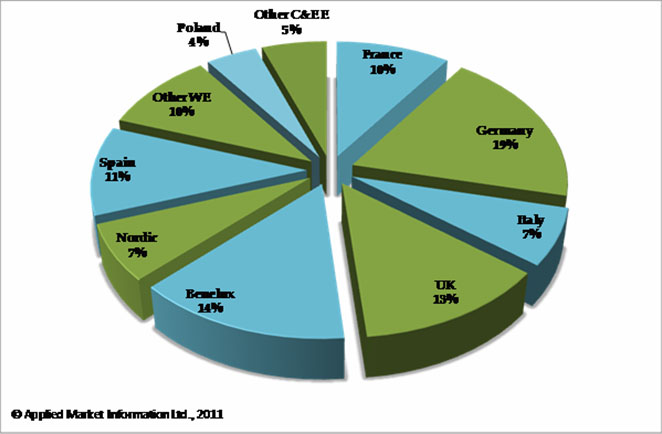

| Plastic sacks now account for over half of all sacks used in industrial packaging in Europe and are set to make significant inroads into markets which up to now have mainly used paper such as cement, pet food and food ingredients, as per a report by Applied Market Information Ltd. The industry has been undergoing a period of significant change driven by an increased competitive dynamic at the customer level, new developments in resin technology and restructuring of European supply. Opportunities but also challenges arise for the plastic sack manufacturers who strive to keep and expand their market share. Total demand for plastic heavy duty sacks in Europe during 2011 was estimated at just over 5,200 million units or just under 600,000 tons. In unit terms plastic sacks now account for over half of all sacks used in Europe. While share is forecast to continue growing market growth has been slowing due to: • Relative maturity of the market. • Increasing use of big bags, FIBCs and bulk deliveries due to consolidation within the sectors downstream in the industry. • Ongoing downgauging trends where still feasible. The most significant growth has been, and continues to be, in the form fill & seal sector (FFS), which now represents 70% of plastic heavy duty sack usage, followed by a 24% share held by open mouth sacks and 6% share held by valve sacks. The share of FFS material is expected to increase in future thanks to the processing and economic benefits it offers, while valve sacks at some point may all but disappear from the market. Open mouth sacks are likely to maintain a relatively stable market share. The largest end use applications for plastic heavy duty sacks are chemicals & fertilizers and horticultural products accounting for just over 30% and 20% of the market respectively. Although these will continue driving the market in volume terms, the end uses with the fastest growing potential are now applications which have been the traditional strongholds of paper sacks including cementitious products and food ingredients (such as flour, milk powder or sugar). These have already seen some shift from paper sacks to plastic and thanks to developments in technology, special closure sack systems and advanced film formulations this trend is forecast to be much more profound in the next five years. The markets are mainly in Germany, Benelux and the UK which take the lead in plastic industrial sack consumption and together account for almost a half of the total European market. While the West European countries will drive the consumption of sacks in tonnage terms, in fact it is Central and Eastern Europe which will have the fastest recorded annual growth rates over the next five years, where penetration levels are much lower LDPE was traditionally the major resin used in the production of heavy duty sacks, however, its use is now in decline, while LLDPE, especially C6 and C8 grades and metallocene resins have been increasing owing to the enhanced performance that these resin grades offer. Thanks to much research and development in resin and technology but also the need for cost cutting and rationalization during the years of the economic crisis between 2008 and 2010, the average thickness of plastic heavy duty sacks has reduced by around 5% between 2009 and 2011. Although it is increasingly difficult to further down gauge film used for sacks the industry will continue to strive for more advanced technologies e.g. pre-stretching (such as MDO) and ever improving film formulations to allow the use of as little plastic as possible so that heavy duty sacks becomes lighter, thinner and therefore more environmentally friendly. Given the strong competition between sack types and the changing industry structure, all stages of the supply chain require a strong level of commitment to the business in order to develop successful strategies. Heavy duty sacks, made of both plastic and paper, have recorded rapid growth in the past two decades. As the market has been reaching maturity, the pace of growth, however, has slowed down significantly, first for paper sacks and in recent years also for plastic industrial sacks.  |

Previous Article

Next Article

{{comment.DateTimeStampDisplay}}

{{comment.Comments}}